The Millionaire Mindset Shift: From Paycheck-to-Paycheck to Purposeful Wealth

- Tony Bradshaw

- Apr 20

- 11 min read

Let me tell you something that took me way too long to figure out.

Growing up in Nashville, in a home where money was always tight, always stressful, and never talked about in any kind of meaningful way, I thought that's just how life worked. You go to work. You get paid. You pay your bills — if you're lucky. And then you do it all over again. Nobody in my world was talking about investing, building wealth, or becoming a millionaire. That wasn't for people like us.

That was the story I carried with me right into adulthood...and I kept doing it until I turned 25.

And here's the crazy part — even after I got a college degree, got a good job as an engineer, and was earning decent money, I was still living that same paycheck-to-paycheck story. Because it wasn't about the money. It was about the mindset.

It wasn't until my mid-twenties that I had a real wake-up call. I looked at my finances and I was embarrassed. I was mismanaging everything. I had no savings, no plan, no vision for what my financial future could look like. And I remember thinking — if something doesn't change, nothing is going to change. I'm broke now, and I'll be broke in the future.

That moment set me on a path that eventually led me to becoming a millionaire by age 40. Not because I got lucky. Not because I had some wealthy uncle who left me money (By the way, that doesn't happen very often). But because I made a choice. I call it the Millionaire Choice. My choice to become a millionaire. And at the center of that choice was something deeper than a budget or an investment strategy. It was a complete mindset shift.

Today I want to walk you through the exact mental shifts that separate people who build wealth from people who stay stuck. These aren't just feel-good concepts. These are real, practical changes in how you think about money — and when you make these shifts, everything else starts to follow.

Shift 1: From "I Can't Afford It" to "How Can I Afford It?"

This might sound like a small thing, but I promise you — it's not.

When most people see something they want or need — a course, an investment, a savings goal — and it feels out of reach financially, they shut the door immediately. "I can't afford it." Full stop. End of the conversation.

That one phrase is one of the most wealth-limiting things you can say, and I'll tell you why. It's not just a statement about your bank account. It's a statement about your belief in your own ability to figure things out.

Rich Dad Poor Dad author Robert Kiyosaki talks about this — the difference between saying "I can't afford it" and asking "How can I afford it?" One closes your mind. The other opens it.

When I started asking how instead of saying can't, things started to shift. I started finding solutions. I started getting creative. I started looking at my income and my expenses differently. I started asking, "What do I need to cut? What can I earn more of? What can I do differently?"

Now listen, I'm not telling you to go spend money you don't have. You don't need another payment. That's not what this is about. This is about developing a problem-solving mindset instead of a defeated one. It's about keeping your brain in the game instead of throwing in the towel before you even try to win.

Most people were never taught this. They were taught to live within their means — and that's not bad advice, but it only goes halfway. The other half is learning to expand your means. You do that by asking better questions and problem solving. There plenty of ways to make more money. You just have to find them.

Start practicing this today. The next time money feels like a wall, don't say "I can't afford it." Ask, "How could I afford this? What would need to be true for me to make this happen?" Even if the answer doesn't come immediately, you've kept your mind open. And an open mind finds opportunities that a closed one never will.

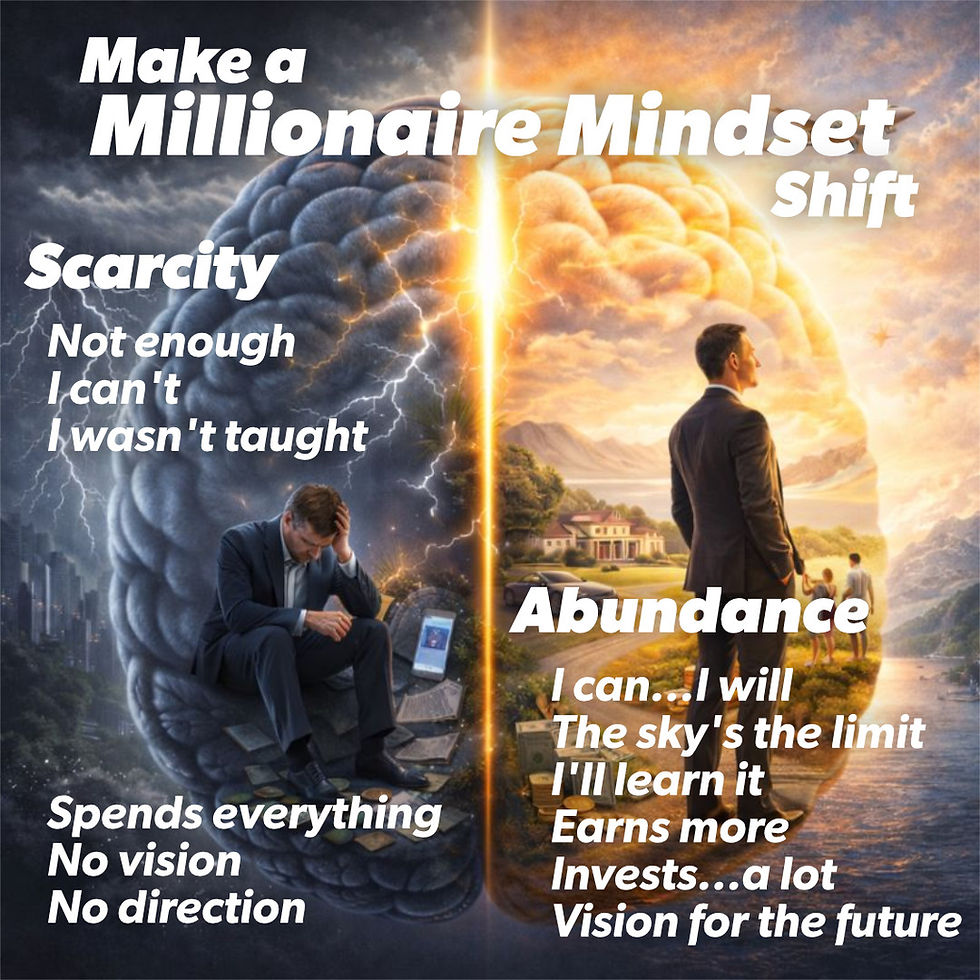

Shift 2: From Scarcity to ABUNDANCE AND Stewardship

Here's one of the biggest things I've learned on this journey: how you think about money determines how you handle money.

Scarcity thinking sounds like this: There's never enough. I have to hold on to every dollar. Money is hard to come by. I don't deserve to have more than I need. People with a scarcity mindset hoard, but they don't build. They fear money as much as they want it.

Abundance and Stewardship thinking sounds completely different: I'm responsible for growing what I've been given. Every dollar I have is a tool. I have the ability to manage, multiply, and give from what I earn.

That shift from scarcity to abundance and stewardship changed everything for me personally.

When I started seeing myself walking in abundance and as a steward of money — not just a consumer of it — I started treating every dollar with more intention. I stopped spending mindlessly. I started asking, "Is this the best use of this resource right now?" I started saving not because I was afraid, but because I was being responsible with what I had.

There's also a spiritual element to this that I don't want to gloss over. For me personally, my faith is a huge part of my relationship with money. I believe that wealth has a purpose — to enjoy life, to help others, to serve something bigger than yourself...to serve God. When you see money through that lens, it stops being something to be anxious about and starts being something to be intentional with. That's what I mean by purposeful wealth.

You see, wealthy people don't just have more money. They think about money more responsibly. They ask, "What is this money for? What is the best thing I can do with it right now?" That kind of thinking — stewardship thinking — is available to everyone, regardless of how much or how little you have today.

Start where you are. Even if you only have $50 to your name right now, you can practice being a good steward of that $50. Because when you're faithful with a little, you develop the habits that allow you to be trusted with a lot.

ShifT 3 : From Consumer to Investor

Let me give you the number one habit that keeps the average American stuck financially: consuming more than they invest.

I don't just mean spending too much — though that's part of it. I mean the fundamental orientation of how most people relate to money. The system is set up to make you a consumer. Every advertisement, every shopping app, every one-click purchase is designed to get you to spend. And most people spend everything they earn — sometimes more.

Wealthy people flip the script. They pay themselves first. They invest before they spend. They think about what their money can do for them over time, not just what it can buy them today.

Now, I grew up understanding consumerism really well. I understood how to spend money. What nobody taught me — and nobody taught most of us — was how to multiply money and make it work for you. How to put money in places where it grows. How to build assets instead of just accumulating expenses.

Here's a simple framework I want you to carry with you: every dollar you earn has a job to do. Some dollars are for living expenses — that's fine. Some dollars are for giving — I believe strongly in that. But some dollars need to be working for you 24 hours a day, 7 days a week, building your future.

When I started allocating money with that mindset — even small amounts — everything changed. Because investing isn't just about money. It's about developing a new identity. When you call yourself an investor, you start making decisions like an investor. You think longer term. You're more patient. You're less likely to blow $200 on something you don't need because you know that $200 is doing something important for your future.

You don't need to start big. Start with whatever you can — even if it's $25 a month into a retirement account. The amount matters less right now than the habit and the identity. You are becoming someone who invests. Hold on to that. And while you're at it, rachet it up. Start with 10% of your income. Then strive to make it 15%. Then 20%. Keep going. Can you get to 50% of your income going into investments?

Shift 4: From "Someday" to "Right Now"

I talk to people every single day who know they need to change their financial situation. They know they need to save more, invest, build a plan. And almost all of them say some version of the same thing: "I'll do it when..."

When I get a raise. When the kids are older. When I pay off this debt. When things settle down. When I have more time.

Here's the hard truth: someday is the most expensive place to live.

The reason "someday" is so costly is a little thing called compound interest. Time is the most powerful force in wealth-building, and every month — every year — you wait is money you will never get back. The person who starts investing $300 a month at 25 ends up with dramatically more money than the person who starts investing $500 a month at 40. That's not opinion. That's math.

But beyond the math, there's something else going on. "Someday" is often fear wearing a disguise. It feels like patience or practicality, but really, it's a way of avoiding the discomfort of starting. Starting means confronting where you actually are. Starting means making some uncomfortable changes. Starting means admitting that you've been waiting too long already.

I want to challenge you today — not someday, today — to do one thing financially that you've been putting off. Open that savings account. Set up that automatic transfer. Look at your budget and identify one expense you can cut. Sign up for that financial literacy course. Make one decision that future-you will be grateful for.

The perfect financial plan that starts tomorrow will always be beaten by a good financial plan that starts right now.

Shift 5: From "I Wasn't Taught This" to "I Am Learning This"

This one is close to my heart, because it was one of the most powerful shifts I made.

I genuinely was not taught how to handle money. Not at home, not in school, not anywhere. And for a long time, I used that as a reason — not intentionally, but subconsciously — for why I wasn't getting it right. Nobody taught me. How am I supposed to know?

And the thing is, that's fair. It's true for most of us. Over 70% of Americans are living paycheck-to-paycheck. That's not because 70% of Americans are lazy or irresponsible. It's largely because our financial education system is broken. Schools don't teach personal finance in any meaningful way. Families that struggle with money pass those struggles — and those beliefs — down to the next generation.

So yes, you may not have been taught. But here's the thing: you're an adult now. And adults who want a different outcome have to take responsibility for their own financial education.

That's actually why I created Get Money Smart and why I wrote 31 Days to Get Money Smart. Because I know that when people have access to real, practical, easy-to-understand financial education, things change. I've seen it happen hundreds of times. The moment someone truly understands how money works — how inflation works, how investing works, how compound interest works — they start making different decisions. They can't not make different decisions. Knowledge is that powerful.

So if you've been using "I wasn't taught this" as a reason to stay stuck, I want to flip that script for you today. You are learning this. You're reading this newsletter right now. You're doing the work. Give yourself credit for that — and then keep going.

Financial education isn't a one-time thing. It's a lifelong habit. The wealthiest people I know are still learning. They read, they listen to podcasts, they talk to other smart people about money. They never stop studying. And neither should you. If you want to be good with money, you have to learn how it works. You have to study money. You have to Get Money Smart.

Shift 6: From No Vision to a Clear Millionaire Plan

Here's something I've observed after years of coaching people on their finances: one of the biggest problems isn't behavior — it's the lack of vision.

People don't have a financial vision. Nobody taught them how to have one. So they're just sort of... existing financially. Paying bills, maybe saving a little, hoping things work out. But there's no destination. There's no plan. There's no moment where they looked at their life and said, "Here's where I'm going. Here's what I'm building toward."

One of the first things I ask people is: what's your millionaire plan? Not just "do you want to be a millionaire?" — but have you written it down? Have you run the numbers? Have you mapped out when you'll get there and how?

When I made my millionaire choice at 25, the first thing I did was create a plan. I mapped out what I needed to save and invest each year. I identified the steps I needed to take. I gave my financial future a clear destination. And that changed everything, because now every financial decision I made was in the context of a bigger goal. It wasn't just "should I buy this?" It was "does buying this get me closer to or further from where I'm trying to go?"

Vision is powerful. When you have a clear picture of where you're headed, your behavior starts to align with that picture naturally. You stop making random financial decisions and start making intentional ones. You become the architect of your financial life instead of just a passenger in it.

I don't care if you're 22 or 52. It's not too late to build a vision and create a plan. The best time to plant a tree was 20 years ago. The second best time is today. Get a piece of paper. Write down a number and a date. "I will have $X by age Y." Then work backward from there. What do you need to save each month? What do you need to learn? What do you need to cut? What do you need to start?

Your millionaire plan doesn't have to be perfect on day one. It just has to exist. You can adjust as you go. The worst plan is the one that lives only in your head and never gets written down.

Bringing It All Together

Let me tie a bow on this, because I want to make sure you walk away with something you can actually use.

The gap between where you are financially and where you want to be is almost never just about income. It's not just about how much you make. I know people who earn six figures and are broke. And I've met people with modest incomes who are quietly building significant wealth. The difference is almost always mindset.

Here's a quick summary of the Millionaire Mindset shifts we've talked about:

From "I can't afford it" to "How can I afford it?" — keep your brain problem-solving instead of shutting down.

From scarcity to abundance and stewardship — see yourself as a manager of money, not just a user of it.

From consumer to investor — give every dollar a job that builds your future. Don't spend your future. Invest it.

From "someday" to right now — time is your most valuable financial asset; stop letting it run out. Get started.

From "I wasn't taught this" to "I am learning this" — take ownership of your financial education. Learn how money works.

From no vision to a clear plan. A millionaire plan. — write down where you're going and map out how to get there.

None of these shifts require a higher income. None of them require a perfect credit score or a financial background or a degree. They require a decision. A choice. Your millionaire choice.

I made mine at 25, in a moment of honest self-assessment where I realized the path I was on wasn't going to take me where I wanted to go. And I want you to make yours — right now, in this moment, as you're reading this. Make your own millionaire choice.

You are not stuck because of where you came from. You are not stuck because of what you weren't taught. You are not stuck because of your current income. You are stuck because of a story you've been telling yourself about what's possible for your life.

Change the story. Change the mindset. Change the outcome.

Virtually anyone can build wealth. I know because I've seen it happen over and over again — from single-parent homes, from low-income neighborhoods, from people who started with nothing but a decision to get money smart...from a 62 year old broke guy to a 69 year old millionaire. It's never too late.

You can do this. I believe that with everything in me. Now go get money smart.

This post offers an interesting perspective on shifting from a paycheck-to-paycheck mentality toward a more intentional and purpose-driven approach to building wealth. I liked how it focuses on mindset change as well as practical financial awareness, especially the idea that long-term wealth is often shaped by habits, discipline, and how people choose to think about money rather than just income level. It also highlights the importance of setting clear financial goals and developing consistency in decision-making, which can be valuable in both personal finance and broader learning areas like MBA Dissertation Topics that explore financial behaviour, entrepreneurship, and strategic planning in real-world contexts.